Understanding the Current Housing Market

Experts describe the current U.S. housing market as facing unique challenges. These challenges have emerged over the nation’s 250-year history since gaining independence in 1776. One significant issue today is the gap between wages and home prices, making homeownership difficult for many Americans.

Data from JP Morgan highlight that home prices have surged by around 60% since the start of the COVID-19 pandemic. Mortgage rates are high and have remained so since 2022. The U.S. homeownership rate dropped to its lowest level since 2019, recorded at 65% last year, according to Census data.

Daryl Fairweather, Redfin’s chief economist, noted the extraordinary nature of the current housing market. Despite mortgage rates not being as high as they were in 1981, when they peaked at 18%, they are higher than average from the past decade. This situation has made housing affordability particularly challenging for young people looking to buy their first home.

The Historical Significance of Homeownership

Homeownership has deep roots in the American identity. Fairweather explains that property ownership was integral to the nation’s foundation. The idea comes from the principles of life, liberty, and property, a concept heavily influenced by John Locke and later reflected in the Fifth Amendment.

Figures such as Thomas Jefferson promoted the independent landowner as democracy’s cornerstone, while Andrew Jackson expanded political participation and encouraged westward expansion. The Homestead Act of 1862 granted settlers 160 acres of public land, often taken from Indigenous peoples, highlighting the appeal of land ownership to immigrants from Europe. This promise of land ownership also significantly structured the U.S. economy’s evolution.

A Broken Promise: What Went Wrong?

American policymakers have long advocated for homeownership as a way to build wealth and fortify the middle class, said Joel Berner, a senior economist at Realtor.com. Homeownership aligns with values of independence and self-reliance, acting as a wealth generator that families can pass to future generations.

Fairweather agrees, citing the belief in America that homeowners constitute the wealthiest class. Nevertheless, the housing bubble burst in 2007-2008 showed the sustainability issues of the system, especially with subprime lending and lax regulation.

Despite past challenges, homeownership remains a critical part of the American dream. A survey from Realtor.com projected that two-thirds of Americans aim to own a home. The tax system further supports homeownership through benefits like mortgage interest deductions.

However, despite the dream, renters face increasing difficulties climbing the property ladder, particularly post-pandemic.

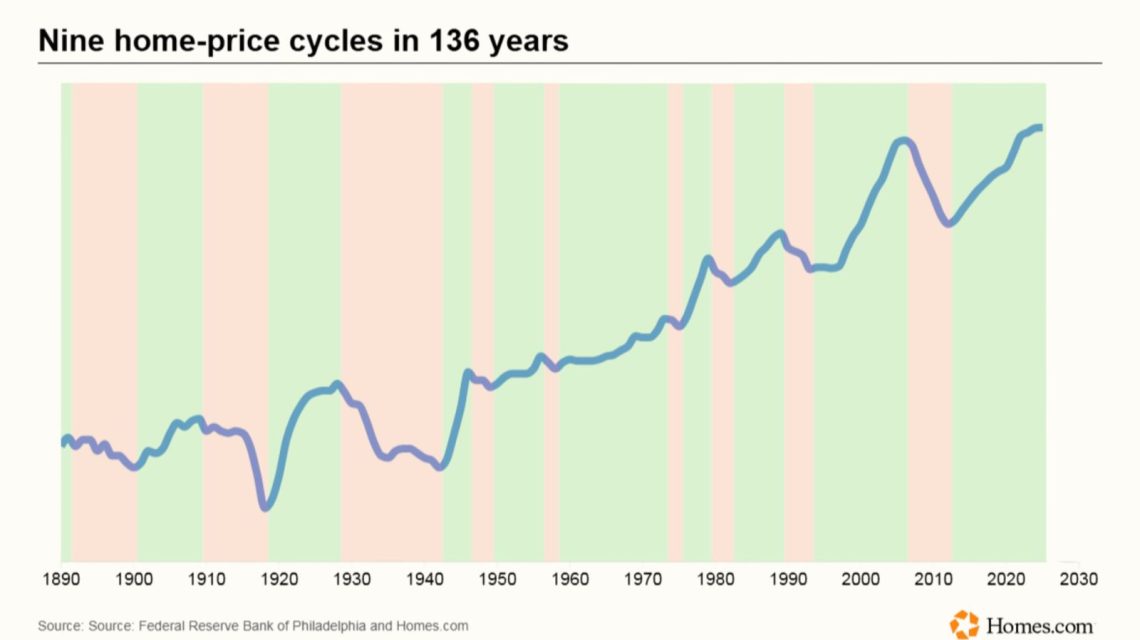

The Origins of the Affordability Crisis

Brad Case, Homes.com’s chief residential economist, traced the roots of the affordability crisis. He noted a shortage of homes and a tendency to view properties more as investments. The introduction of the 30-year fixed-rate mortgage by the government in the 1930s eased homebuying for millions, improving accessibility.

However, mortgage rates soared alongside inflation in the 1970s and 1980s, pushing house prices beyond the rise in incomes. Some viewed home purchases primarily as investments, fueling public policies that advanced house prices faster.

The current resistance to building affordable houses stems from existing homeowners’ preference for expensive developments, which attract higher taxes. This dynamic emerged over recent decades.

Seeking Solutions for the Housing Market

The post-pandemic housing market remains uncertain. During the pandemic, mortgage rates dropped, leading to a buying frenzy. Subsequently, rates doubled, making the market appear stuck. Homeowners with record-low mortgage rates resist selling, while prospective buyers face high prices and rates.

The market this year has seen a slow spring despite a surplus of sellers compared to buyers. Most sellers quickly delist homes, indicating reluctant engagement with buyers.

Fairweather pointed to an anomaly where home prices typically fall as mortgage rates rise, but now, both supply and demand have reduced. Berner remarked the market is facing structural challenges akin to conditions before the Homestead Act in reducing regulatory barriers for new construction.

Yet, experts see possible future affordability improvements. In some regions, like the South and West, prices are adjusting, while areas in the Northeast and Midwest continue struggling with inventory shortages.

Baby boomers, owning a considerable share of homes, may slowly make homes available, aiding younger buyers. However, Fairweather warns of rising maintenance costs tied to older homes and climate change.

Ultimately, addressing affordability requires focused income growth and a shift in homebuying attitudes toward residence rather than investment, Case advises.

While housing may become more affordable later, efforts toward a sustainable and affordable market will continue.

Addressing the Affordable Housing Crisis: Challenges and Solutions

Addressing the Affordable Housing Crisis: Challenges and Solutions  U.S. Housing Market Sees Falling Prices Amid Economic Concerns

U.S. Housing Market Sees Falling Prices Amid Economic Concerns  First Bank of the United States Reopens as Museum

First Bank of the United States Reopens as Museum  San Francisco Home Overrun by Squatters Sells Quickly Despite Poor Condition

San Francisco Home Overrun by Squatters Sells Quickly Despite Poor Condition  Minnesota Sues Seller for Predatory Practices Against Somali Muslim Homebuyers

Minnesota Sues Seller for Predatory Practices Against Somali Muslim Homebuyers  GoHealth Co-Founder Clint Jones Lists Lincoln Park Mansion

GoHealth Co-Founder Clint Jones Lists Lincoln Park Mansion